The DAT-ification of everything: The risk/reward of ETFs, treasuries, and index wrappers

As bitcoin and crypto assets get wrapped into ETFs, treasuries, and digital asset trusts (DATs), the market is becoming more accessible — and more fragile. This week’s volatility shows how quickly those wrappers can turn into points of failure.

Strategy Inc. has always been a weird public company. Originally a sleepy enterprise software firm, it pivoted hard into bitcoin in 2020 and never looked back.

By 2025, it had effectively shed any pretense of software relevance and rebranded into what it is now: a public wrapper for bitcoin, powered by leverage and Michael Saylor’s Twitter account.

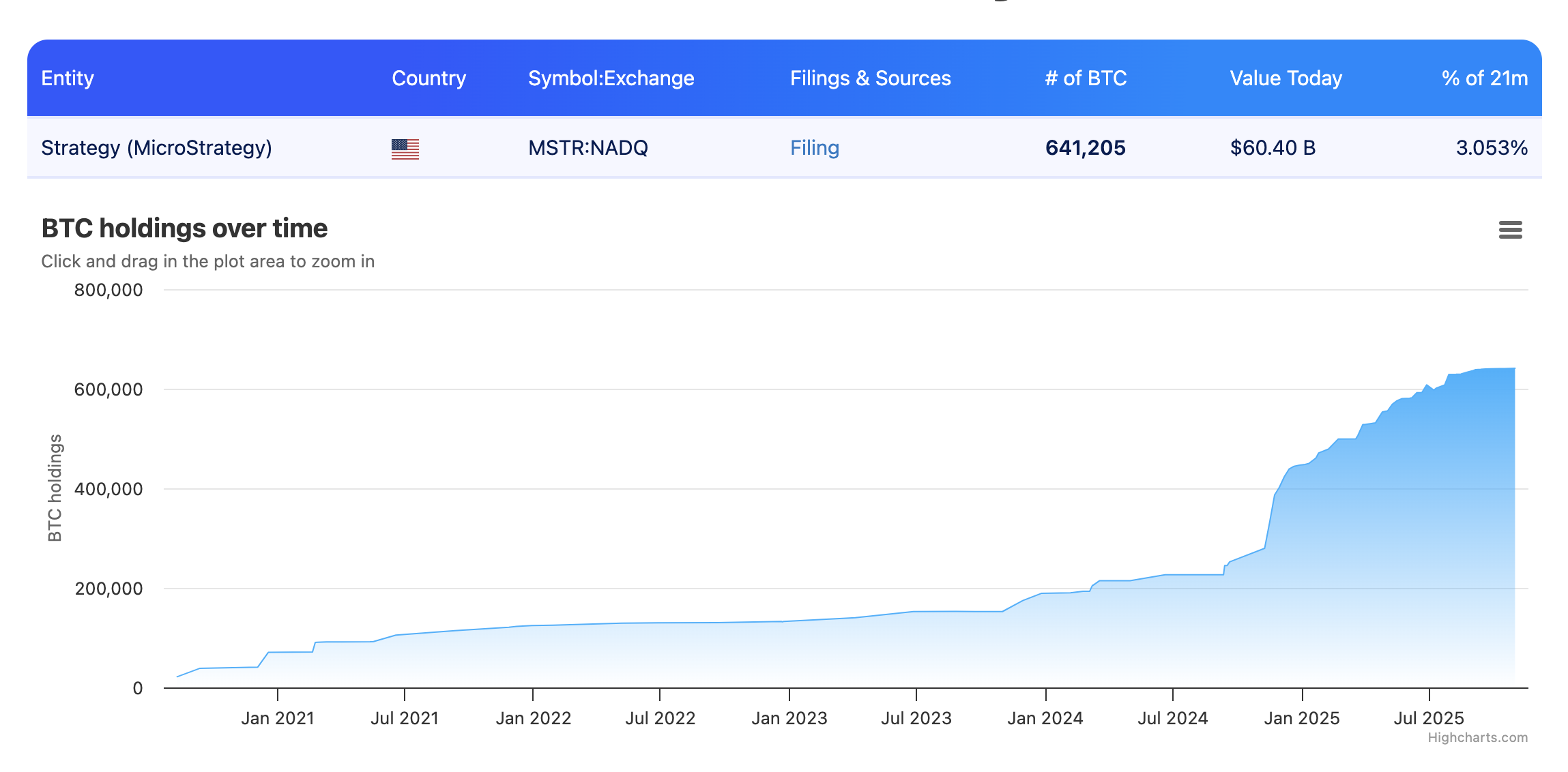

As of this week, Strategy holds over 640,000 BTC, which is more than 3% of all the bitcoin that will ever exist, and more than most ETFs, sovereign entities, or exchanges. It’s second only to Satoshi himself on most ownership leaderboards. This hoard made the company famous. It also made its stock a kind of volatility-maximized bitcoin derivative: part ETF, part meme, part hedge fund, all risk.

That worked beautifully during the 2024–2025 rally. At the peak, Strategy’s market cap exceeded the value of its bitcoin by nearly $80 billion. Investors were pricing in not just the coins, but the leverage, the optionality, and whatever aura you want to assign to the company that seemed to always be buying bitcoin.

Then the market energy started receding.

This week, bitcoin dropped below $95,000. Strategy’s stock dropped even faster. For the first time in years, its market cap fell below the fair market value of its treasury — meaning investors were valuing the whole enterprise, leverage and all, at less than the sum of its coin parts.

The meme version of this is that Strategy turned into a slightly jankier, more volatile version of a spot ETF that started trading at a discount. The serious version is that one public company’s financial structure has become so central to bitcoin’s liquidity and narrative regime that its equity premium is now a stress indicator for the broader market.

And this was a stress week.

Rumors, flows, and thinning books

Spot ETFs saw $870 million in net outflows on Nov. 13 alone, the second-largest daily exit since their debut. Zoom out to the week of Nov. 3–7 and the picture’s worse: billions left crypto ETFs across both BTC and ETH, reversing weeks of bullish inflows and triggering rebalancing across risk books.

Liquidity wasn’t there to catch the fall. Kaiko data showed bitcoin order-book depth had dropped from $766 million in early October to just over $535 million this week. Less depth means less capacity to absorb large flows without moving price. And this week, the flows were large.

Enter the Saylor subplot. Onchain analysts flagged a sharp drop in BTC tagged to Strategy, from 480,000 to the low 400,000s. That number didn’t line up with Strategy’s own disclosures, which still showed over 640,000 BTC on the books. This kicked off a full-blown rumor cycle: was the “never sell” company quietly dumping?

Saylor responded by saying said Strategy was buying, not selling. But whether the wallets were mis-tagged or the rumors were wrong isn’t the point.

The point is that one company’s wallet tags now move the market.

Which raises a bigger problem: when the structure of the market is so concentrated that rumors about one actor can trigger price spirals, you’re not dealing with an antifragile system. You’re dealing with a fragile wrapper around a supposedly decentralized asset.

Strategy is a bespoke digital asset trust

Strip away the branding and Strategy is basically a customized, publicly traded digital asset trust (DAT). It holds bitcoin. It issues a security. It uses debt and equity to lever up its position. Investors buy the stock not for the legacy business, but for the coin exposure.

Newer crypto ETFs operate on the same basic model: pool coins, wrap them in a security, let the market price the wrapper. At times, these wrappers trade at massive premiums or discounts to the underlying asset. At times, they become liquidity sinks or sources of volatility.

The key difference is scale and structure. Strategy is a single-corporate-balance-sheet version of this. It is not regulated like a trust, but functionally it does the same thing. It absorbs bitcoin and issues claims.

So do formal DATs. Wyoming has a digital asset trust charter. The Department of the Treasury is reviewing applications for national trust banks focused on crypto. ETFs now wrap everything from bitcoin to dogecoin.

Strategy, in this sense, is the outlier. It's a legacy DAT wrapped in a corporate shell, offering leverage and opacity at the cost of liquidity risk. When things go well, it’s an efficient way to bet on bitcoin. When the premium flips and leverage bites, it becomes a systemic vulnerability.

Building a DAT-shaped market

Bitcoin isn’t alone in this drift. The entire market is tilting toward wrappers.

Spot ETFs hold a growing share of circulating BTC. So do corporates like Strategy and Metaplanet. Seeking Alpha recently noted that the float, or the actual amount of bitcoin that trades freely, is shrinking as large, slow-moving entities accumulate. Meanwhile, ETF flows are becoming increasingly violent: $500 million in one week, $1.2 billion out the next.

Sovereign wealth funds, endowments, and family offices are piling into DAT-like products instead of touching spot. The surface structure looks like adoption. Underneath, it’s a consolidation of control.

That doesn’t make the networks themselves fragile. The bitcoin protocol clears blocks whether the ETFs are net buyers or net sellers. Ethereum still processes transactions whether ETH ETFs are trending or not. But the financial layer on top, the place where most capital interacts with crypto, is increasingly built on a few giant wrappers.

And wrappers, unlike protocols, have balance sheets. They have redemptions. They have debt.

Remember antifragile?

The original appeal of network money was that it could survive chaos. Taleb’s “antifragility” was about systems that grow stronger from volatility. The recipe: decentralization, redundancy, and distributed failure.

Bitcoin-the-protocol has that. Bitcoin-the-asset-in-2025 does not.

Ownership is concentrated. Market structure is intermediated. Liquidity is shallow. The biggest holders aren’t multisig collectives or DIY cypherpunks, instead they’re ETFs, corporates, and trust banks. And when those wrappers wobble, the whole asset class can feel it.

That’s not a death sentence. It’s just a reality check. The more we financialize the asset, the more the asset behaves like finance. And finance, even with bitcoin as its base layer, comes with redemption risk, duration mismatch, and the occasional mass deleveraging.

This week was a taste of that.

Open Money: Wrappers aren’t the asset

The Open Money view is that the core question isn’t price, or even adoption. It’s structure. Who holds the keys? Who sets the rules? Who bears the risk when things go sideways?

On that front, DATs and corporate treasuries are tools, not outcomes. They’re useful for distribution — a way for institutions to allocate to crypto without leaving their comfort zone. But they are not the end state.

If the future of digital assets is just a handful of mega-wrappers, we’ve rebuilt the legacy system on new rails. The illusion of decentralization won’t protect you from correlated risk when all the wrappers get hit at once.

Strategy isn’t bitcoin. ETFs aren’t the network. They’re scaffolding. And scaffolding should never be mistaken for the building itself.

So by all means, buy the ETF. Trade the stock. Bet on the premium.

Just don’t confuse the wrapper with the money.