The Superchain Reckoning

Base's February 2026 departure from Optimism's OP Stack, followed by its March 31 strategy roadmap doubling down on tokenized markets and stablecoin payments, is the clearest signal yet that sovereignty, not shared governance, is the structural winner.

Summary: On February 18, 2026, Base announced it is migrating from Optimism's OP Stack to a unified, in-house codebase — a single base/base GitHub repository and client, with node operators required to migrate ahead of upcoming hard forks.

Base's March 31, 2026 strategy roadmap builds directly on this technical independence, prioritizing tokenized asset markets, stablecoin-native payments, and developer and AI-agent tooling as the explicit focus for the year ahead.

The departure ends Base's revenue-sharing arrangement with the Optimism Collective — a fund that Base had, in practical terms, almost entirely financed. This piece argues that Base's exit is not a defection from open financial infrastructure.

It is the predictable outcome when a permissionless L2 reaches sufficient scale that coordination overhead becomes a liability, and it reveals something structural about how open money infrastructure actually matures: through sovereign, purpose-built execution layers anchored to Ethereum's transparent settlement — not through perpetual shared governance committees.

The Open Money lens

The Open Money Framework evaluates financial infrastructure across three layers — settlement (how value moves), intermediation (lending, trading, yield, tokenization), and coordination (governance, onchain identity, public goods) — and five dimensions of openness: permissionless access, transparent verification, programmable logic, composable infrastructure, and sovereign custody.

Before jumping into the latest, it might be helpful to get caught up on Base and to learn more about why what we'll cover below is significant.

Base's move primarily occupies the settlement layer at the composable infrastructure dimension, with a secondary signal in programmable logic.

The OP Stack was designed as a composable infrastructure primitive: any chain could fork it, benefit from shared sequencer upgrades, and contribute to and draw from a common public-goods pool. Base's departure tests the boundaries of that model.

The question is not whether the OP Stack succeeded as composable infrastructure — it demonstrably did, having launched hundreds of chains and processed enormous economic activity.

The question is what happens to shared infrastructure when one participant's scale makes collective governance structurally inefficient.

Last weekend's edition examined a parallel dynamic at the governance layer: what happens when corporate product wrappers are removed from coordination infrastructure, and whether public-goods funded tooling can replace VC-backed SaaS. The Base/Superchain situation is the same structural question applied one layer down, at the settlement rails.

What happened

The OP Stack launched with a specific thesis: a shared, open-source L2 framework would allow chains to benefit from collective security, shared upgrade velocity, and a revenue-sharing mechanism that funded Ethereum public goods through the Optimism Collective. The vision was the Superchain — a horizontally composable network of L2s with interoperable state and sequencer economics flowing into a common pool.

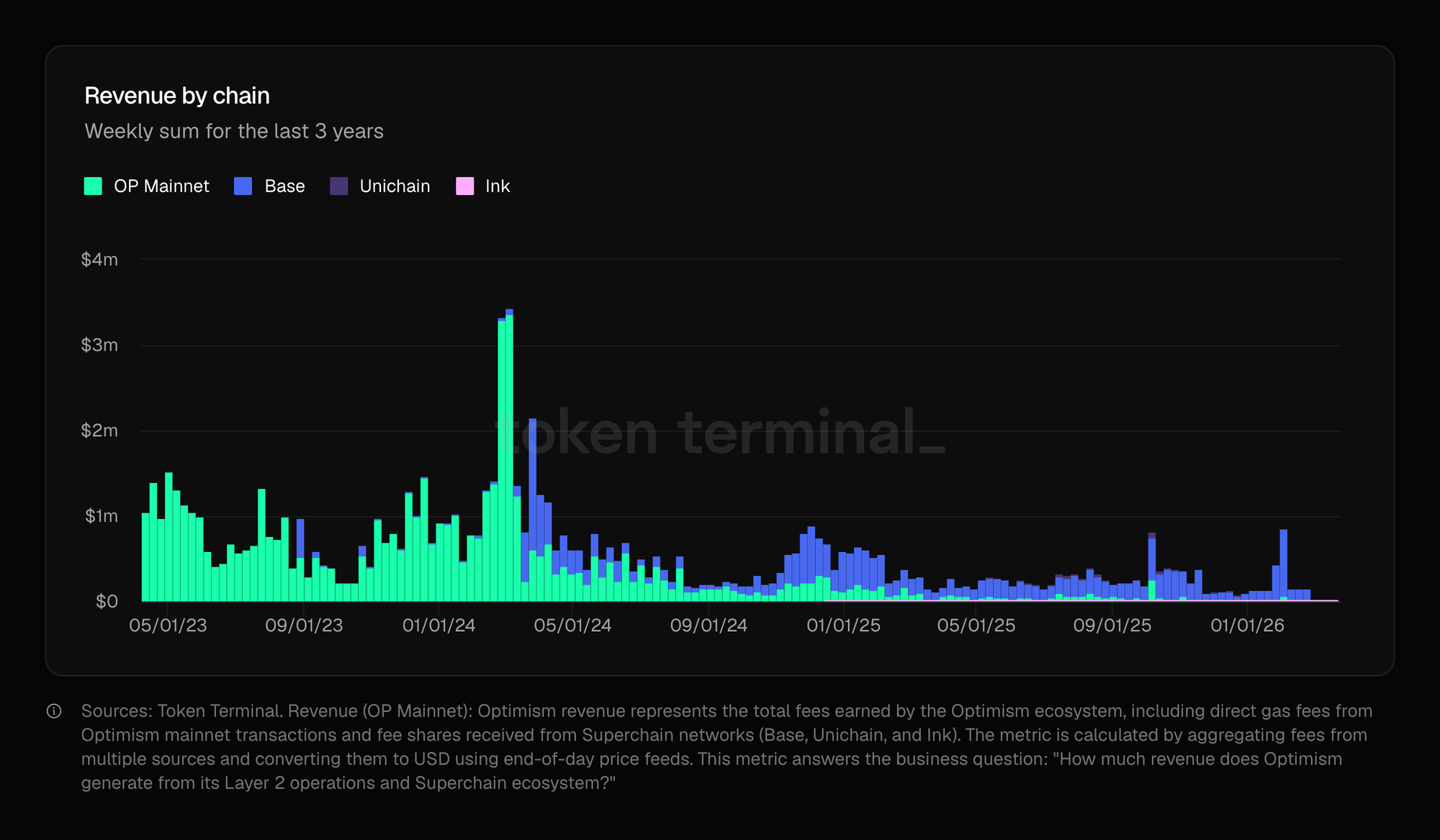

Base joined the OP Stack in 2023 and grew faster than every other Superchain participant combined. By late 2025 and into early 2026, Base was contributing between 70 and 96.5 percent of the sequencer fees flowing to the Optimism Collective — approximately 8,387 ETH out of roughly 14,000 ETH in total lifetime inflows. It was funding the majority of OP token buybacks, the retroactive public goods funding program, and the operational overhead of OP Labs. The Superchain's public goods model was, in practice, a Base subsidy program with governance framing applied over it.

The February 18 announcement made the economic logic explicit. Base cited the need to double its hard fork cadence — from approximately three major upgrades per year to six tightly scoped ones — as a primary driver. It also cited the need to move to faster TEE (Trusted Execution Environment) and ZK finality proofs on a timeline that the shared OP Stack upgrade schedule could not accommodate.

The unified codebase removes the overhead of cross-chain coordination for every upgrade decision. Base will continue to upstream bug fixes and will retain OP Enterprise support contracts, but revenue sharing ends.

The March 31 roadmap makes clear what Base intends to do with that additional speed: tokenized asset markets (equities, commodities, Treasuries), stablecoin-native gas fees, and AI-agent accounts — what the roadmap describes as agent-native infrastructure.

The Revenue Reality

The economic impact on the Optimism Collective is not a background detail. It is the structural consequence that makes Base's exit meaningful rather than merely technical.

The Optimism Collective's revenue model depended on Base at the level of a primary funding source. The OP buyback mechanism, which has operated as the main value accrual vehicle for OP token holders, was predominantly capitalized by sequencer fees — fees that Base generated at rates no other Superchain chain approached.

OP Mainnet itself, the flagship chain of the Superchain, generated sequencer revenue at a fraction of Base's throughput. In the months before the February announcement, Base's DEX volume ran approximately 144 times that of OP Mainnet.

The practical consequence is that the Optimism Collective loses its primary engine at the same time it faces operational pressure. OP Labs reduced its headcount in March 2026, a contraction that analysts have directly connected to anticipated revenue loss from the Base exit. The OP token's reaction to the announcement reflected this: OP fell materially on the announcement day, and has not recovered to pre-announcement levels in the period since.

Shared infrastructure funded by sequencer revenue-sharing works when revenue is distributed broadly enough that no single participant's exit creates a structural hole. When one participant generates the majority of the revenue and reaches the scale where shared governance imposes real costs, the model breaks along the seam that was always there.

The Superchain's public goods vision required that Base's growth remain slower than its coordination overhead — a condition that was never guaranteed and did not hold.

The upgrade velocity case

The velocity argument deserves its own treatment because it is the one that will determine whether Base's bet pays off at the roadmap level.

Operating on the shared OP Stack, Base was constrained to the upgrade cadence that the Superchain's governance process could support — approximately three major hard forks per year, coordinated across chains with different operational priorities and client implementations. Six hard forks per year, tightly scoped and custom-engineered for Base-specific infrastructure needs, represents a fundamentally different development model. The comparison is not between fast and slow; it is between sovereign iteration and federated iteration.

The practical difference becomes visible when mapped against the March 31 roadmap. Tokenized equities and commodities settling on Base require custom ERC standards, reliable fast finality, and the ability to deploy protocol-level changes in response to regulatory and market structure changes on timelines measured in weeks, not quarters.

Stablecoin gas requires changes to the fee market that are Base-specific and would require cross-chain coordination votes if implemented under the Superchain model. Agent-native accounts require new account abstraction primitives that Base wants to ship ahead of broader Ethereum ecosystem consensus. None of these are achievable at OP Stack cadence.

The projected shift from optimistic fault proofs to TEE and ZK finality proofs is the most technically significant change in the roadmap. Optimistic proofs carry a seven-day challenge window — a finality delay that is acceptable for speculative DeFi activity but creates real friction for institutional tokenized asset transfers, where counterparties need finality confirmation to complete settlement.

TEE and ZK finality, once deployed, reduces that window to near-instantaneous. The implication for tokenized markets is direct: Base's upgraded finality model makes it meaningfully better infrastructure for institutional RWA settlement than any optimistic-proof L2 operating on a shared upgrade schedule.

The thesis stated and tested

The central claim of this piece is: open financial infrastructure matures through sovereign, purpose-built L2s that retain permissionless access and programmable logic while sacrificing maximal shared composability — because institutional speed and control now matter more than collective revenue-sharing once a chain dominates usage.

The evidence supporting this is the full arc of Base's economic history on the Superchain. Permissionless participation does not require perpetual revenue subsidy once scale is achieved.

The OP Stack gave Base a production-grade starting point, sequencer infrastructure, and legitimacy within the Ethereum ecosystem. Base's departure does not repudiate any of that — it simply recognizes that the model's benefits were front-loaded, and the ongoing costs of shared governance have exceeded the marginal benefits of remaining in the federation.

The Ethereum settlement anchor is what makes the sovereignty argument coherent. Base is not leaving Ethereum; it is strengthening its Ethereum-anchored finality by moving to faster proof mechanisms. Transparent verification at the base layer — Ethereum mainnet — remains intact.

What Base is departing is the smaller federation of Superchain chains that sit above Ethereum, not Ethereum itself. Sovereign L2s are not closed systems. They are specialized execution environments that compose with Ethereum's open settlement layer while operating their own programmable logic without coordination drag.

What the counterarguments reveal

Interoperability friction is real and underdeveloped

Base's exit reduces cross-chain composability with remaining OP Stack chains. DeFi protocols that had been building on the assumption of seamless Superchain interoperability — shared state, standardized messaging, direct token bridges — now face a fragmentation that was not in their model.

Liquidity that aggregated across OP Mainnet and Base under shared infrastructure assumptions now needs bridge infrastructure or cross-chain messaging to move between them.

This is a real constraint. The Superchain's value proposition included a vision of atomic composability — transactions that could span chains without the user experience overhead of bridging. That vision is deferred or reduced by Base's departure. The remaining Superchain chains retain interoperability with each other, but they lose the economic throughput that made the federation's shared sequencer revenue meaningful.

The honest read is that the fragmentation risk rises for DeFi applications built on cross-Superchain composability, while falling for institutional tokenized asset use cases that were never going to rely on Superchain-specific bridges for settlement anyway.

Smaller chains lose the rising tide

The Optimism Collective's public goods model was designed as a rising-tide mechanism: Base's success would fund improvements in infrastructure, developer tooling, and research that benefited every chain on the Superchain, including smaller ones that could not independently fund protocol-level research.

With Base's sequencer revenue gone, the question is how those smaller chains sustain themselves.

The answer that the Optimism ecosystem is likely to develop is a version of the same answer that independent protocols have always found: direct protocol treasury funding, external grants, and developer communities motivated by users rather than by a shared revenue pool.

These are not inferior to the shared model — they are the default mode for every successful protocol that has not been inside a revenue-sharing federation. The adjustment is painful and the timeline is uncertain, but the endpoint is not structurally worse for chains that were only marginally dependent on Superchain revenue to begin with.

Institutional compliance perception

Enterprises onboarding to tokenized asset infrastructure may initially view a shared, coordinated L2 federation as lower-risk from a governance and liability standpoint than a sovereign chain operated by a single company's engineering team.

The compliance perception question is not trivial. Coinbase has significant institutional relationships and regulatory standing that other L2 operators do not. The question is whether Base's security council changes — the addition of independent signers announced alongside the February migration — are sufficient to satisfy enterprise governance requirements, or whether institutional clients will require additional reassurance about upgrade key management and protocol-level changes.

The independent signers change is a direct response to this concern. It is not a perfect answer, but it represents a deliberate recognition that sovereign control and institutional trust are not automatically in opposition. The trajectory of Base's governance structure over the next 12 months — how transparent upgrade governance becomes, how independent the security council actually operates — will determine whether this concern proves material or manageable.

Where the matrix stands after Base

The Open Money Framework's settlement layer, composable infrastructure dimension, has been the most active cell in the matrix over the past 24 months.

The OP Stack's rise filled much of that cell with demonstrated, production-scale evidence. Base's departure introduces new conditions.

Permissionless access at the settlement layer is unaffected by Base's departure. Base remains permissionless by construction — anyone can deploy a contract, anyone can send a transaction, anyone can run a node. The permissionless property is not a governance feature; it is a protocol-level property that sovereignty does not change.

Transparent verification improves under Base's roadmap. ZK proofs, once deployed, allow anyone to verify the state of Base's execution layer against Ethereum's settlement layer without trusting Base's sequencer. The upgrade from optimistic proofs to ZK proofs is a direct improvement in the transparent verification dimension.

Composable infrastructure narrows. Cross-superchain composability contracts. The remaining OP Stack chains gain a more coherent internal composability layer as Base's departure simplifies their governance, but the overall composable infrastructure score for the broader ecosystem reflects a real reduction in atomic cross-chain capability.

Programmable logic advances. Base's 2026 roadmap is a programmable logic expansion: stablecoin gas fees, tokenized asset ERCs, agent-native account abstractions. These are new primitives that increase what money can be programmed to do on Base's execution layer.

The trade-off is that they are Base-specific rather than Superchain-wide, which limits composability while advancing the frontier of what is programmable.

Research backlog

What is the actual state of Base's security council independence? The February announcement cited the addition of independent signers to the security council as a governance improvement. The composition, voting thresholds, and operational independence of those signers are not yet publicly detailed at the level required to assess whether this represents meaningful governance decentralization or a nominal change with Coinbase retaining effective unilateral control. This is the single most important governance question for institutional clients evaluating Base as RWA settlement infrastructure.

What happens to Superchain interoperability post-Base? The remaining Superchain chains — OP Mainnet, Mode, Zora, and others — retain shared infrastructure and sequencer coordination. The practical question is what their economic model looks like without Base's sequencer revenue. OP Labs has not published a revised sustainability model. Understanding whether the remaining Superchain can self-fund its development and public goods commitments without Base requires a detailed analysis of the remaining chains' fee generation and OP Labs' cost structure post-headcount reduction.

When do TEE and ZK proofs deploy on Base mainnet, and what finality guarantees do they provide? The March 31 roadmap describes TEE and ZK finality as a 2026 priority without committing to specific deployment dates. The finality improvement from optimistic proofs (seven-day challenge window) to ZK proofs (near-instantaneous) is the most consequential technical change for institutional tokenized asset use cases. The deployment timeline determines when Base's infrastructure becomes materially better than current alternatives for RWA settlement.

What ERC standards is Base planning for tokenized equities and commodities? The March 31 roadmap identifies tokenized markets as a priority without specifying the technical standards it intends to support or introduce. ERC-3525 (semi-fungible tokens), ERC-1400 (security tokens), and custom transfer restriction schemas all have different trade-offs for equity tokenization. Base's choice of standards will determine which institutional players can compose against its infrastructure without additional middleware, and which will require bridging solutions that reintroduce the friction that custom finality was designed to remove.

Does Base's exit accelerate or delay Ethereum L1's role as a universal settlement anchor? The theoretical case for Ethereum as the open settlement anchor improves when individual L2s strengthen their Ethereum finality rather than building competing settlement layers. Base's ZK proof upgrade is consistent with this thesis. The question is whether a pattern of sovereign L2s anchoring to Ethereum creates a more durable settlement architecture than the shared Superchain model would have, or whether fragmentation at the L2 layer eventually pressures L1 settlement assumptions.

Can the Optimism Collective's public goods model survive without Base's revenue? The Optimism Collective's RPGF (Retroactive Public Goods Funding) program has been one of the more credible experiments in protocol-level public goods funding in the Ethereum ecosystem. Without Base's sequencer revenue, its continued operation depends on either OP Mainnet's fee generation recovering to fund the program independently, or a structural change to how the Collective is capitalized. The answer to this question matters beyond Optimism: RPGF is a model that other ecosystems have watched and partially replicated. If the model proves unsustainable without a dominant fee-generating chain, it changes the calculus for public goods funding across the broader ecosystem.