When buy now, pay later moves onchain

Klarna is launching KlarnaUSD, a fiat-backed stablecoin built on the Tempo blockchain to reduce cross-border payment costs. This marks a shift toward stablecoin-based settlement infrastructure, as fintechs begin replacing legacy rails like SWIFT and card networks with programmable money.

Klarna is a Swedish payments company best known for its buy now, pay later services and e-commerce checkout integrations. It operates across Europe and the United States, processing billions in retail transactions annually for consumers and merchants.

If you shop on the internet at all, you've probably noticed Klarna buttons at checkout. The big news this week is that Klarna is launching its own US dollar-backed stablecoin.

While the new stablecoin is called KlarnaUSD and it's designed more as internal infrastructure for payments and not the typical consumer-facing asset. The company plans to use the coin to improve how it settles transactions, starting with cross-border flows and merchant payouts.

KlarnaUSD will be fully backed by fiat reserves and issued using Stripe’s Bridge infrastructure. The coin will run on a new blockchain called Tempo (KlarnaUSD is currently in testnet), which was built by Stripe and Paradigm specifically for regulated payments.

KlarnaUSD is currently being tested in limited environments. Klarna expects to expand the rollout to more users and regions by 2026. The big takeaway here is that the checkout flow doesn’t change. The shopping app stays the same. What changes is how money moves once a payment is initiated, and this is that aspect that makes this the most interesting to the Open Money framework.

In some ways, Klarna rolling out stablecoins as payment infrastructure is more evidence that a massive pivot toward programmable money is underway. Klarna is a large and established player, with about $100 billion in gross merchandise volume per year. The company's decision to issue its own stablecoin indicates that these technologies are finding a place inside mainstream fintech platforms.

A payments decision, not a crypto product

Stablecoin adoption is increasingly tied to payment use cases. Cross-border payments alone generate around $120 billion in fees annually. Klarna plans to use KlarnaUSD to reduce those fees by avoiding traditional settlement methods like SWIFT or card networks.

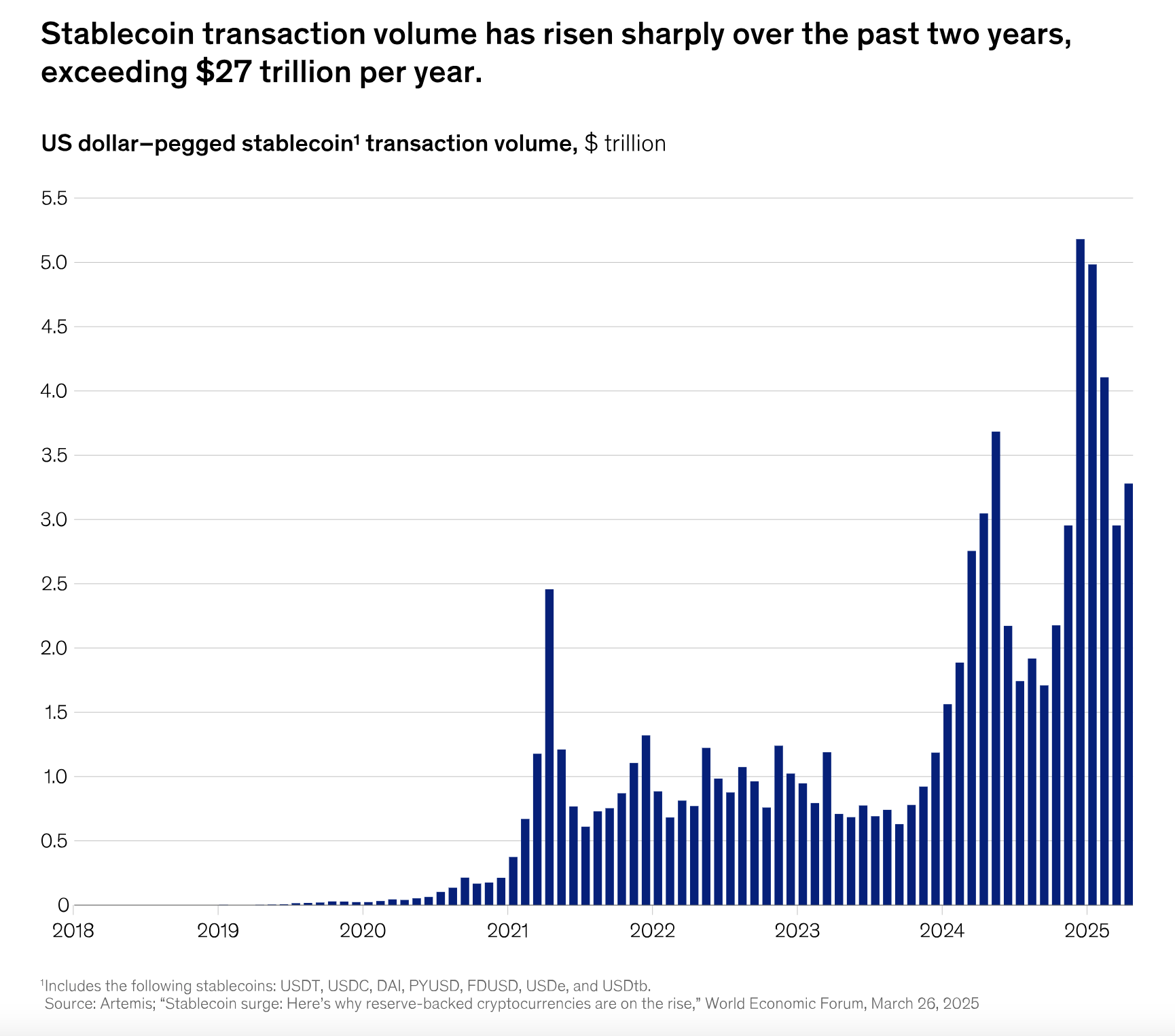

Stablecoins already move more than $20 trillion per year in onchain transfers, and this number continues to grow. McKinsey and other research firms now treat stablecoins as a serious component of future financial infrastructure. (Source linked in the graphic below).

The operational benefits are clear. Using KlarnaUSD allows Klarna to reduce its reliance on third-party rails. This can lower costs, shorten settlement times, and improve liquidity by allowing funds to move at any time of day, including weekends.

Klarna also gains more control over the transaction stack, which opens up new design possibilities for how it handles payouts, FX, reconciliation, and treasury operations. These changes do not require consumer education or user onboarding. They operate at the infrastructure layer, below the interface.

Regulatory clarity is enabling stablecoin issuance

Klarna’s ability to launch its own stablecoin is supported by new legal frameworks in both the US and the EU.

In the United States, the GENIUS Act creates clear rules for issuing fiat-backed stablecoins. In Europe, the Markets in Crypto-Assets (MiCA) regulation outlines a regime for e-money tokens. These frameworks give Klarna and other licensed entities the ability to create stablecoins without ambiguity around reserves or oversight.

With regulatory structures in place, established fintechs are beginning to experiment with issuing their own digital dollars. KlarnaUSD is one example. PayPal USD is another. Stripe’s involvement through Bridge and Tempo adds a third layer to this activity. Klarna’s move signals that programmable dollars are becoming part of the standard toolkit for modern financial companies.

Tempo as payments infrastructure

The chain KlarnaUSD runs on is called Tempo. It was built by Stripe and Paradigm to serve the needs of regulated financial institutions. Tempo supports fast settlement, compliance tooling, and native stablecoin issuance. It uses blockchain mechanics, but its governance and architecture are tailored to institutions, not public networks.

KlarnaUSD on Tempo doesn’t require merchant adoption or user switching. The coin can be used internally to settle Klarna's own operations, and over time it may be extended to partners.

The infrastructure is designed to be programmable and composable, but the environment is curated and regulated. This reflects a design choice: create a blockchain that supports modern financial operations without the volatility or openness of general-purpose public chains.

A broader shift in who controls digital dollars

The launch of KlarnaUSD is part of a wider trend. Fintechs are beginning to issue their own branded stablecoins and integrate them directly into their platforms.

PayPal USD was an early example. Stripe’s Bridge tooling is helping others follow. KlarnaUSD joins this landscape as one more version of a private, programmable dollar distributed through an existing consumer platform.

This shift affects how money moves and who controls the path it takes. Fintechs with strong distribution and existing merchant relationships can begin to settle more of their own volume directly. This reduces their dependency on card networks and banks, and allows them to design their own economics around settlement and liquidity.

The implications extend to infrastructure providers. When stablecoins begin to replace portions of SWIFT and Visa settlement, the business model for legacy rails comes under pressure.

Questions for Open Money

Open Money has tracked the rise of programmable financial systems that live below the surface. KlarnaUSD is a case study in how that shift looks when it arrives inside a large consumer fintech.

The tools being used — stablecoins, composable payment rails, onchain settlement—are the same as those explored in public crypto markets. The difference is the context. Klarna is integrating these tools into regulated infrastructure, designed for operational efficiency and payment optimization.

The Open Money framework raises a few open questions around developments like this:

- Interoperability: As more companies issue their own stablecoins, the payments landscape could begin to fragment. KlarnaUSD, PayPal USD, and other branded coins may not be compatible unless shared standards emerge.

- Governance: Tempo is blockchain-based but tightly governed. This presents a structural design question. Future financial infrastructure may be programmable, but not neutral.

- Resilience: KlarnaUSD depends on reserve quality, auditability, and risk management. Stablecoin designs vary widely in how they address these questions. Even fully-backed coins introduce dependencies that require oversight.

- Regulatory scope: The frameworks enabling this shift are new. Regulatory adjustments or political shifts may introduce new constraints. What is allowed today may become restricted under future conditions or changes in administrations.

These questions do not diminish the significance of what Klarna has done. They frame the context for understanding how proprietery stablecoins are likely to evolve from here.

A structural shift with quiet signals

KlarnaUSD was not introduced with a major marketing campaign. There is no splashy launch interface. The coin is not aimed at retail traders. The design is practical, backend-oriented, and operational.

That approach aligns with where programmable money is starting to find traction. Not in speculative markets or experimental DeFi apps, but in enterprise-scale financial operations that require new tools for cost reduction, speed, and flexibility.

Klarna’s decision to issue a private stablecoin signals that digital dollars are no longer an external innovation waiting to be integrated. They are becoming part of the foundation layer for how value moves inside large financial systems. The Open Money thesis has pointed toward this shift for some time. The KlarnaUSD launch is one more confirmation that the transition is underway.