When memes move markets

A fictional 2028 memo about an AI-driven crisis rattled real markets. Not because it revealed new facts, but because it offered a coherent plot investors could trade. In a memetic market structure, narrative velocity shapes price — and programmable settlement rails start to look less optional.

Earlier this week, a post titled “The 2028 Global Intelligence Crisis” moved through the market like a stress signal. It was written as a macro memo from June 2028. The post was explicitly fictional and explicitly a thought experiment, and not designed as a market forecast.

It still hit.

That alone is instructive.

Markets price more than cash flows; they also price coordination. A fictional memo can become catalytic if it provides a narrative that feels coherent, arrives at the right moment, and compresses uncertainty into something tradable.

This week’s Citrini memo worked on two levels:

- as a case study in narrative propagation as market structure and the power of memetics

- as a quiet validation of an Open Money premise: if commerce becomes agent-driven and machine-settled, the settlement rails matter, and stablecoins appear not as ideology but as infrastructure.

Part I: The memetics layer

What happened

Citrini and Alap Shah published a long-form scenario describing an “intelligence displacement spiral” in which AI productivity scales faster than income distribution, creating pressure in credit markets, housing, private assets, and politics.

It circulated quickly, like memes do. The post became screenshots, then group chat fodder, and then news outlets started covering the fictional post that actually moved markets.

If you don't have time to read the entire thing, here's a pretty good summary:

For the entirety of modern economic history, human intelligence has been the scarce input. Capital was abundant (or at least, replicable). Natural resources were finite but substitutable. Technology improved slowly enough that humans could adapt. Intelligence, the ability to analyze, decide, create, persuade, and coordinate, was the thing that could not be replicated at scale.

Human intelligence derived its inherent premium from its scarcity. Every institution in our economy, from the labor market to the mortgage market to the tax code, was designed for a world in which that assumption held.

We are now experiencing the unwind of that premium. Machine intelligence is now a competent and rapidly improving substitute for human intelligence across a growing range of tasks. The financial system, optimized over decades for a world of scarce human minds, is repricing. That repricing is painful, disorderly, and far from complete.

Attention as part of price discovery

The structural shift underneath all of this is simple: attention now moves faster than institutional response.

What matters is not only the information itself, but the coordination layer around it.

A narrative that is legible will often outrun one that is technically correct but cognitively expensive. A narrative that lands when positioning is fragile will outperform one that arrives too early. A narrative that screenshots well will travel farther than one that requires caveats.

AI accelerates this layer by creating more summaries, more reframing, and more instant synthesis. The result is more pressure to form consensus quickly. Narrative propagation becomes a transport protocol for markets.

“When memes move markets” is not metaphor. It is a description of the structure of how things work now.

Part II: the Open Money layer

Why stablecoins appear in the footnotes

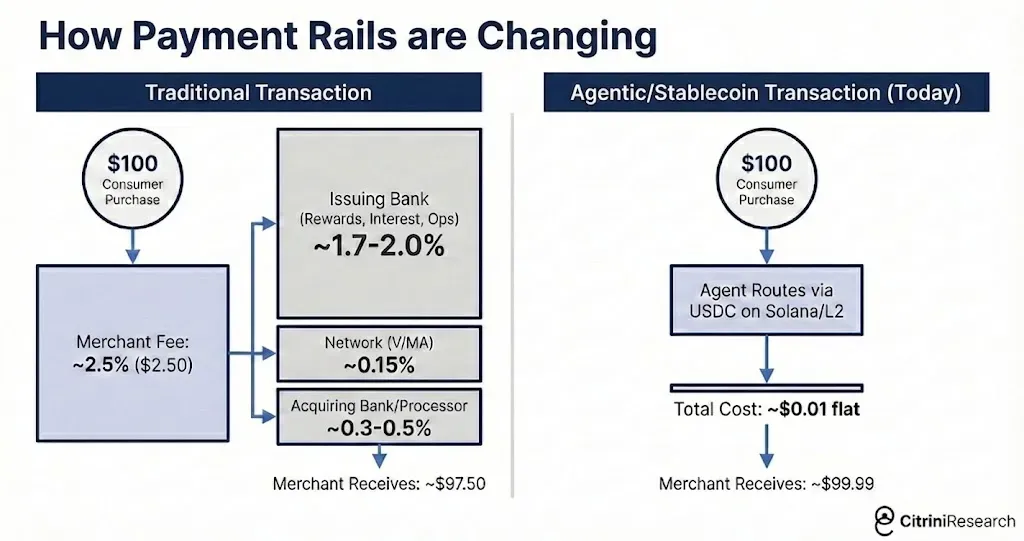

One subtle move in the Citrini scenario is that stablecoins show up as plumbing. As agents optimize routing and reduce friction, the memo gestures toward stablecoins on fast chains and L2s as obvious settlement rails: cheap, near-instant, programmable.

That framing aligns with an Open Money thesis: the monetary layer is increasingly defined by settlement capabilities. The future winners will be the systems that can clear value efficiently under new conditions.

If machine-to-machine commerce expands, several implications follow:

- Payments become a software surface

- Settlement becomes an optimization problem

- Infrastructure that is global and programmable becomes default

Stablecoins are not guaranteed winners. But today they function like APIs for dollars, and they are composable and programmable (two big components that define Open Money). These properties matter if counterparties become software agents.

Stress testing institutions versus primitives

Open Money is not a macro forecast. It's more of a design system to ensure resilience and sustainability in the future as the information age quickly morphs into the intelligence age.

If transactions become machine-generated, if counterparties are software, if participation is global and pseudonymous by default, then financial primitives must operate without assuming slow human coordination or trusted intermediaries at every step.

That does not resolve distributional issues or neutralize political risk. And an Open Money system doesn't inherently mean stability or even ease of use.

But it does, at least for now, clarify the research program.

Also, somewhat related, and possibly of interest: I wrote a rebuttal to a guest essay that appeared in the New York Times earlier this week. The guest essay tries to build the argument that crypto has no point.

— Daniel McGlynn (@danielmcglynn) February 27, 2026

Research backlog

- What makes a narrative tradable: legibility, timing, distribution, or author credibility?

- If attention is endogenous to market structure, what are the failure modes? Narrative bank runs. Reflexive sell-offs triggered by synthetic consensus.

- If agents transact autonomously, which settlement rails dominate: upgraded card networks, stablecoins, API-accessible bank deposits, or something else?

- If stablecoins become infrastructure, where do the chokepoints sit: issuers, chains, wallets, compliance layers, liquidity venues?

- How do financial systems build narrative resilience? Through transparency, auditability, circuit breakers, or broader market literacy?

Closing thought

The striking detail this week was not that a fictional memo unsettled people.

It was that this felt structurally normal. History is filled with stories of markets melting down because of real events. But have we seen a market meltdown because of a portrayal of fictional events two years in the future? It might be a first.

Markets increasingly trade narratives that propagate faster than underlying adjustments can occur. The distance between story and price is compressing, which is one of the hallmarks of a memetic market structure.